The recent speech by Turkey’s President, Recep Tayyip Erdoğan, about exchanging U.S. Dollars for Gold and the Turkey Lira caught my attention. I immediately recalled the reports about Basel III requirements, currency wars, digital currency, the global reset, and the De-dollarization campaign.

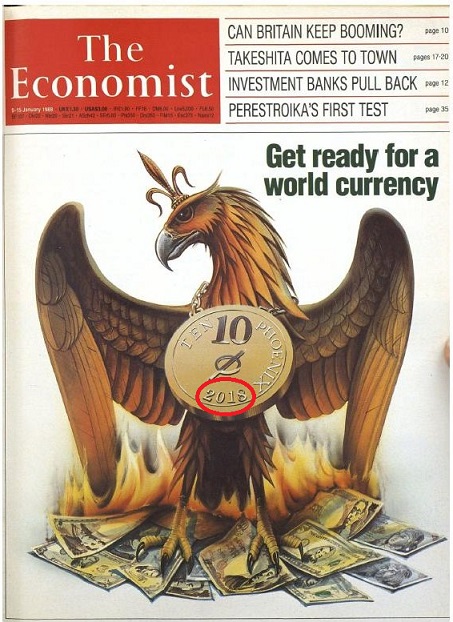

Among conspiracy researchers and truth seekers the 1988 cover of the ECONOMIST magazine predicting changes to the world’s monetary system in 2018 can not be forgotten:

Few in America know of these institutional activities that are implementing worldwide monetary changes, and the likely effects on national currency valuations.

The New Rules Have Gone Into Effect.

Recently the world has witnessed disasters on the Bolivar and Rupee currencies, and I expect other currencies will experience volatility in their valuations.

Below are reports from around the world about the banking gold standard, Capital Requirements, and Liquidity Standards.

Remember, your deposits into the banks are no longer yours, it immediately becomes property of the banks and the government. Please discuss and share this, because what is coming is no accident, it is Policy! ~Ron

∇

Few appreciate that the launch of a Shari’ah gold or Islamic gold [6] standard signals a changing dynamic in the gold market. Gold bullion will be additionally appealing to Islamic banks due to Basel III rules that require banks own high liquidity and quality, low counter party risk assets such as physical gold in allocated and segregated storage [7].

Until now, no group as influential as the AAOIFI has issued guidelines stating that gold must be the underlying asset in all gold transactions as we suspect they will do shortly.

Whilst the likes of the COMEX gold market are able to grow to multiple times the size of the underlying physical market, with little impact on physical demand or price, this will no longer be case.

Jan Skoyles is a research executive at GoldCore, a gold investment platform and this is a version of an article that first appeared in the Khaleej Times [8], the UAE’s best selling English newspaper and highest circulated English language newspaper in the Gulf –zerohedge.com

Shariah

English: Islamic jurisprudence

Alternate spelling: Sharia, Shari’a, Shari’ah, Syariah, Syaria, Syari’ah, Syari’a

Definition: Islamic cannon law derived from three sources: the Quran, the Hadith and the Sunnah

A “Shariah compliant” product meets the requirements of Islamic law.

A “Shariah board” is the committee of Islamic scholars available to an Islamic financial institution for guidance and supervision in the development of Shariah compliant products.

A “Shariah advisor is an independent Islamic trained scholar that advises Islamic institutions on the compliance of the products and services with the Islamic law.

§

The AAOIFI and the World Gold Council have vowed to create new gold-traded products and markets in Islamic finance, as the former launched a new Shariah standard to guide the industry in trading the precious metal. Traditionally, gold has been treated as a currency in Islamic finance which has confined its use to spot transactions, but fresh guidance from AAOIFI is expected to spawn a wave of product development in the industry, reported Reuters.

In May this year, it was reported that global gold demand reached 1,290 tonnes in the first quarter of 2016, a 21% increase compared to the same period in 2015, making it the second-largest quarter on record, according to the World Gold Council’s Gold Demand Trends report. This increase was driven by huge inflows into exchange-traded funds (ETFs), fueled by investor concerns regarding economic fragility and an uncertain financial landscape. In line with this, the new gold standard is believed to spur interest among industry players to develop gold-based products and consequently spark increase investment in gold and structured products and ETFs backed by gold.

In summary therefore, ETFs based on gold and the increased development of investment products would be welcome in the Islamic finance industry in general, but its growth and impact on the overall industry depends on the development of other regulatory and practice-related governance and transparency. What is most certain is that the demand for such new products is there and investing and saving in gold is a well-rooted culture and custom in the Middle East, Asia and other parts of Muslim societies, which in practical terms constitutes a good ground base for an industry to flourish and prosper.

However, industry stakeholders, together with other standard-setting bodies, will need to work more closely to develop an efficient ecosystem for this promising niche market.

Dr Hatim El Tahir is the director of Islamic Finance Knowledge Center at Deloitte & Touche Bahrain. He can be contacted at heltahir@deloitte.com.

§

GLOBAL: In less than two days since AAOIFI and the World Gold Council (WGC) released their long-awaited Shariah standard on gold, international platforms, including a fintech firm, have formally announced their plans to launch Shariah compliant gold solutions in a race to capture the individual and institutional wealth of increasingly affluent Muslim populations which for years have been hesitant to invest in the yellow metal due to complexities and lack of clarity over the asset class.

Newly-minted Kuala Lumpur-based fintech firm, HelloGold, for example, which was the first online gold platform to be endorsed as Shariah compliant by Amanie Advisors – the force behind the AAOIFI standard – confirmed that it is expanding its reach beyond Malaysia to include other ASEAN markets in the second half of 2017.

“For many in Asia, gold is a particularly good safe haven investment against foreign exchange risk and market shocks such as we have seen in 2016. Over the last 12 months, gold has risen by 17% against the Malaysian ringgit, 10% against the Thai baht, 9% against the Indonesian rupiah, 17% against the Philippine peso and 12% against the Singapore dollar,” explained Robin Lee, CEO of HelloGold and formerly CFO of WGC.

The fintech firm aims to democratize access to investments and savings by removing the cost hurdle to individual investors – offering customers the ability to buy, sell, save, send gold and use it as collateral from as low as RM1 (22.47 US cents).

In Ireland on the other hand, longtimer GoldCore has begun work on engineering a Muslim-friendly solution, with plans to bring it to market by the first quarter of 2017.

“For a number of years, we have been working on an institutional gold platform and indeed a Shariah compliant gold bullion solution for the institutional market,” said Stephen Flood, CEO of Gold Core, which has offices in the UK, the US and Ireland. “We look forward to launching our comprehensive Shariah compliant gold investment solution and offering it to qualifying Islamic financial institutions in 2017.”

§

INDONESIA: Otoritas Jasa Keuangan (OJK) has granted two licenses to set up a Shariah business unit to venture capital firm Mitra Bisnis Keluarga Ventura and finance company MNC Guna Usaha Indonesia, according to separate statements.

§

With slightly more than a month to go before the end of the year, optimism that the Sukuk market will exceed RAM Ratings’s projection of approximately RM100-120 billion (equivalent to approximately US$23-28 billion based on the exchange rate of US$1 = RM4.3) (RAM expects RM100-120 billion of domestic Sukuk issuances this year as stated on the 23rd March 2016) is high. In the first 10 months of 2016, a record RM115 billion (US$26.7 billion) of Sukuk was issued, hitting RAM’s full-year projection for the local currency market.

Impetus for this year-on-year (y-o-y) growth came primarily from quasi-government (+163%) and corporate (+52%) Sukuk issuances. The underlying sectors were Islamic financial institutions (37% of total quasi-government and corporate issuances) tapping the Sukuk market to meet their capital requirements and infrastructure projects (31% of total quasi-government and corporate issuances) – a trend that dates back to 2014.

From total Islamic debt securities issued, government securities accounted for 34% while quasi-government and corporate issuances made up 25% and 41% respectively. In total, Shariah compliant securities constituted 55% (equivalent to RM115 billion) of the market’s total bond issuances of RM210.9 billion (US$49 billion). With the build-up in Sukuk issuance for the same period, outstanding Sukuk represented 57% (US$156.2 billion or RM671.7 billion) of the total bond market’s RM1.2 trillion (US$275 billion).

In October 2016, US dollar-denominated Malaysian Sukuk were included in the EMBI Global Diversified Index. Coupled with the visibility provided by the incorporation of Malaysia’s government investment issues (GII) into Barclay’s Global Aggregate Index in March 2015, Malaysian Sukuk issuances have gained significant recognition among international investors. This is underlined by the 198% y-o-y surge in foreign holdings of GII to US$7 billion as at the end of October 2016.

Malaysia’s economic pump-priming through infrastructure-led projects has been a boon to the Sukuk market and is likely to remain a key catalyst. Issuances by the quasi-government and corporate sectors are expected to continue playing a significant role in expanding the breadth and depth of the domestic Sukuk market.

Ruslena Ramli is the head of Islamic finance at RAM Rating. She can be contacted at ruslena@ram.com.my.

§

Some of the world’s fastest-growing economies are feeling the strain. Across Asia, currencies have tumbled, exports have weakened, inflation has risen and borrowing costs have shot up in tandem with a rising US dollar with an exodus in emerging market bonds and a wave of capital outflows. But is the news all bad, and how long will it last? LAUREN MCAUGHTRY looks at the landscape for Islamic asset management in the region, and discovers that a few bright spots remain on the horizon.

Turbulent times

The MSCI AC Asia Pacific ex Japan Index has fallen by 4.1% over the last three months. The S&P Pan Asia Shariah Index lost 5.65% over November alone. Emerging markets are taking a beating and Southeast Asia, which has survived well over the pressures of the past year, is finally feeling the consequences. The US election results brought a wave of concern to the region — as US interest rate fears rise, overseas investors have begun to offload Indonesian and Malaysian bonds, which has prompted (and exacerbated) a sell-off that has seen central banks scramble to protect their plummeting currencies.

The asset management industry has not been immune, and Asian funds have been hit badly by the latest events. “The Asian region has been weak since Donald Trump won the US presidential election,” confirmed Akmal Hassan, the managing director of Asian Islamic Investment Management (AIIMAN), to IFN. “The day after the election result were announced, we saw huge fund outflows (amounting close to US$30-40 billion) from emerging markets… back into developed markets.”

And the future remains uncertain. “Investing within the region is expected to remain challenging as uncertainties persist,” agreed David Ng, the chief investment officer of Affin Hwang Asset Management, speaking to IFN. “The vulnerability of the region against possible policy changes by the new US administration could lead to further volatility.”

Islamic prospects

Yet within these turbulent times, some Islamic funds are not only performing well but are seeing inflows into the market. AIIMAN’s top-performing fund is the Affin Hwang Aiiman Asia (ex Japan) Growth Fund — which registered a year-to-date growth of 8.76% as of the 6th December (according to Bloomberg) and has grown 2.6% over the past month alone.

And while some funds may have stumbled due to the recent headwinds (the Aberdeen Islamic Malaysia Equity Fund, for example, is down 4% over the past month and has grown just 1.22% over 2016), others are still flocking to the region, suggesting that investor appetite has not yet dissipated. Hong Kong-based Mirae Asset Management, for example, recently launched its first Shariah compliant product with the Mirae Asset Islamic Asia Sector Leader Equity Fund, targeting European customers and designed to achieve long-term capital growth by investing in Islamic equities across Asia.

So what are the pitfalls facing Islamic funds in the region today — and how can they avoid these issues to ensure performance for their investors?

Currency pressures

Currency pressures are of course the biggest concern — and the two biggest Islamic finance markets in the region have been the worst hit in the recent sell-off. Over the last three months, the Malaysian ringgit weakened by 7.2% against the US dollar while the Indonesian rupiah lost 3% in value over the same period as foreign investors flee the local bond markets as yields spike following Trump’s victory.

With an estimated 40% of Malaysian sovereign bonds and around 35% of Indonesian sovereign bonds owned by overseas investors, this has had a catastrophic impact on the market — and on bond and Sukuk funds. The CIMB Islamic Sukuk Fund has dropped by 1.6% over the past month (as of the 5th December) while the Manulife Dana Sukuk Fund and the Maybank Malaysia Sukuk Fund have both fallen 2.2% over the same period.

With currency reserves estimated at around US$100 billion compared to short-term external debt levels of US$128.2 billion (according to the latest IMF figures), Malaysia is one of the most vulnerable countries in the region to currency attacks and capital outflows, making investors even more wary.

And recent central bank moves to clamp down on currency speculation, including a (largely ignored) request to foreign banks to stop trading in ringgit offshore forwards, have failed to inspire confidence — spurring fears of new capital controls and a fixed exchange rate last seen almost 20 years ago during the Asian financial crisis in 1998 — while the low oil price and continued political scandals are also dragging on performance. Indonesia too has taken steps to intervene, with the central bank supporting the local currency and bond markets through more conventional methods to provide liquidity.

Immediate effect

The future does not look bright, with over US$200 billion pulled from global equity funds since the start of 2016 including US$100 billion in the third quarter alone (according to Morningstar and the FT) — the worst year for equity managers since 2011. In its latest results, emerging markets fund manager Aberdeen Asset Management noted GBP32.8 billion (US$41.75 billion) in net outflows for the year including GBP4.8 billion (US$6.11 billion) for the Asia Pacific region.

According to the latest fund flow report from MIDF Equity Research (as of the 5th December), foreign investors fled the Malaysian market last week with a selling spike of RM487.6 million (US$109.7 million) on the 30th November to reach a cumulate year-to-date exodus of RM2.2 billion (US$494.94 million). Indonesia also saw equity outflows last week of US$237.1 million. “The flow out of Asian equity continued on last week as global funds made a general retreat for the sixth week in a row,” confirmed MIDF. “Funds classified as ‘foreign’ were, in aggregate, net sellers of stocks in six out of the seven Asian exchanges.”

Optimistic impact

So what impact has this had on Asian asset managers?

“The recent ringgit depreciation changed our outlook heading into 2017, as prices of goods and services will be higher going forward. We have experienced this earlier this year and in that instance, the depreciation was short-lived. However, this time around, we anticipate that the currency depreciation will last a little longer,” warned Akmal.

But it is not all doom and gloom — and fund managers are surprisingly optimistic as to their long-term prospects. “As an Asia-focused asset manager, our Asian portfolios have continued to hold up well — which we attribute to risk management and the ability to reduce market exposure during market uncertainties,” Ng explained to IFN. “While the sell-down post-US election has dragged down stocks across the region, our higher cash levels have provided a decent buffer going into the correction. The higher liquidity that the funds held also provided opportunities to buy on weakness.”

And despite the foreign exodus, the market is supported by local investors who retain a regional preference. “We still think there is a general home bias when it comes to investment where familiarity wins out,” said Ng. “We think that investment portfolios remain tilted toward the domestic and Asian region, with a tactical allocation into other selective markets.”

“The worst-performing sectors this year have been the telecommunications and technology sectors, as these experience heavy price competition. Moreover, the performance in the technology sector was dampened with production cuts. We saw performance impacted due to fund outflows from large cap stocks, while mid-cap space suffered as a result of poor results season recently. The construction sector, utilities and exports remain the key performance drivers in our portfolios,” added Akmal. “As it stands, Malaysia and the wider emerging markets region do not benefit from US dollar appreciation. Having said that, there are opportunities for companies in the emerging markets that have a large manufacturing base to have extra gains from the appreciation… Demands for Asian assets remain good as Asian companies continue to offer growth as well as decent dividend yields.”

Under pressure

Another silver lining is the recent OPEC deal to reduce oil production, which pushed up most emerging Asian currencies last week and should support oil exporters such as Malaysia although the ringgit continues to underperform the rupiah, suggesting that the general concern has spread beyond oil.

“We expect a slower growth environment for a prolonged period of time,” agreed Akmal. “Growth in Malaysia will depend on its currency and the global oil price. The recent decision from OPEC to reduce production has helped improved oil prices by 7% to US$50 per barrel, which will help Malaysia in its oil exports. Additionally, corporates in Malaysia stand to gain if the ringgit holds steady at the current levels.”

But although funds have put up a good fight, the continued headwinds are inevitably affecting their performance. “Islamic equities on the domestic front have been under pressure this year,” warned Ng. “The generally smaller investment universe has made it challenging for fund managers, leaving most funds within the category with weaker performance compared to conventional peers. The regional Islamic funds have performed relatively better, given the larger and more diversified universe that [they are] able to participate in. The performance of our regional equity funds have been comparable, and our regional Islamic equity fund is within our top five performing equity funds.”

Akmal agreed. “Performance for Islamic funds for 2016 so far has been weak due to poor market conditions, which also affected the conventional funds. Performances of Islamic funds are also influenced by geographical exposure, ie Malaysia-centric funds underperformed the regional funds.”

An Asian growth story

So what can we expect for the future? Will the continued pressures push down performance, or will Asia remain a bright spot for Islamic asset management?

Jad Shams, the head of MENA at Mirae Asset Global Investments, is bullish on the region’s growth prospects. “No diversified portfolio investor, whether institutional or retail, can afford to be absent the Asian growth story,” he insisted to IFN. “Asia represents the bulk of hard economic assets in the world, driven mainly by its young and aspirational demographics, rapid GDP growth and consumption behavior. Compared to developed markets, Asia’s capital markets are much smaller although Asia owns most real economic assets in the world today. This gap will bridge over time.”

Shams suggests that despite the headwinds, asset management in the region will be supported by continued interest from overseas, especially from GCC investors keen to take a long-term view. “Middle East sovereign wealth funds were among the first international investors in Asia (some with experience going as far back as the 1950s), and they enjoy among the largest foreign investor quotas in India, China, and other Asian markets. So too have other investor segments been investing in Asia for decades. The Middle East is part of Asia and knows Asia’s potential. There will always be demand for Asian exposure by Middle East investors, and many institutions maintain offices with [a] direct presence in Asia, a trend in fact on the rise today.”

Rahul Chadha, the co-chief investment officer at Mirae Asset Global Investments in Hong Kong and the manager of the new Shariah compliant fund, agrees with this perspective. “We still see Asian equities as attractive,” he told IFN. “From the macro fundamental point of view, Asian countries are generally a lot stronger than they were in 1997 (Asian financial crisis), 2007 (global financial crisis) and 2013 (Taper tantrum) in terms of foreign exchange reserves and current account balance. Asian currencies are now very competitive at multi-year low levels versus the US dollar.”

Looking ahead

The outcome of the US election may have come as a surprise to many, but in fact its drivers (and its outcome) are being echoed across the world, with the dissatisfaction of the voting public in weak growth, limited jobs, low wages and widening inequality finding expression in the election of unconventional leaders — such as Rodrigo Duterte in the Philippines, Narendra Modi in India and Joko Widodo (popularly known as Jokowi) in Indonesia. The trend started before Trump, and his election has only highlighted the gravity of these issues. So what does this mean for investors, and what can we expect for the coming year?

“The impact of US president-elect Trump’s victory on performance will ultimately boil down to fund flows, valuations and growth. Foreign funds have mostly exited Malaysia and emerging markets for now, and will return once the currency is undervalued and growth returns,” warned Akmal. “2016 has been a washout year for many companies in Malaysia. This led to lower or flat earnings growth, which then led to expensive valuations. 2017 will start off from a low base and will give the market a chance to reset expectations and grow earnings.”

Cautiously optimistic

And while Asia might be struggling in some areas, in others it holds the advantage. Although global growth is recovering, structural issues in developed markets such as the US and Europe are holding back development — while Asian economies such as India, Indonesia and the Philippines, with their low household debt levels, attractive demographics and strong impetus for reform, are proving attractive to asset managers. “In these domestic-oriented economies, we are generally more pro-cyclical, favoring sectors such as financials, autos and cement,” explained Chadha. “In globally-oriented cyclical economies, we prefer companies with sustainable visibility, staying very stock-specific through companies with technological and brand leadership. In China, we are avoiding banks and deep cyclical sectors, and prefer exposure through internet/e-commerce, tourism, insurance and healthcare.”

While currency is one of the primary considerations for investing in Asia, it must also be remembered that many other factors contribute — including country fundamentals such as demographics, balance of payments and leverage levels; industry characteristics such as barriers to entry, competitive landscape and structural trends; and mostly importantly company-specific drivers such as technological/brand leadership and management quality — all of which play a major role in determining an investor’s return. “Asia is home to some of the most dynamic economies where innovative companies are driving growth in ‘new economy’ industries. This provides exciting investment opportunities for bottom-up investors,” confirmed Chadha.

So could we see an improvement in 2017? Ng is optimistic. “Currency markets are inherently difficult to predict and the conviction level of getting it right consistently is generally very low,” he warned. “However, given the 45% correction in three years, we do intuitively think that the ringgit is undervalued — fundamentally, value should be south of 4.00 levels. Post the sell-off, we are optimistic that focus will shift back onto the fundamental attribution of the respective stocks. We are optimistic that there will still be investment opportunities to be found in respective markets. Fiscal spending will likely intensify within the region as the slow growth environment continues to loom over global economies. The speed and how we adjust to the prevailing market conditions will be the key differentiating factor when it comes to managing funds.”

§

The global financial markets continue to be rocked by political and economic challenges, with the repercussions of the US elections sending shockwaves especially through emerging markets, which are struggling to adjust to the new normal. This week, our cover story takes an in-depth look at the impact on the Asian region, which has seen an exodus from overseas investors and a catastrophic crash in currencies. But are there bright spots on the horizon and how have these elements affected the performance of Islamic funds? Read on for a detailed analysis with insight from some of the top fund managers in the region.

Our IFN reports this week bring you a varied and appetizing selection: from an interview with the CEO of Securities and Investment Company on her outlook for next year, to an exploration of the exciting new Arab-Africa Trade Bridge; while we also bring you our renowned monthly global summary of the overall Islamic markets and our latest update on sovereign Sukuk. Our fund focus looks at the new Shariah compliant offering from Mirae Asset Management, while our case study explores the recent sovereign issuance from Bahrain. Our country analysis looks at Thailand and our sector analysis explores the latest news on corporate governance for Islamic finance.

Our IFN Correspondents bring you news from India, Tunisia, Brazil, South Africa and offshore centers, as well as updates on risk management, Islamic crowdfunding, debt capital markets and Islamic law in Europe. Our feature contributions come to you this week from Bernadette Ngara of the National Bank of Kenya on the growth of Islamic finance in Kenya; Dr Yusuf Abdul-Jobbar of Madinah Islamic University on Shariah governance challenges; and Walid Ghaith of Aljazira Capital in Saudi Arabia on positive drivers for Islamic asset management.

With such an action-filled issue in store for you this week, we apologize in advance to those unable to get any work done while they are glued to our jam-packed pages!

§

As global investors continuously search for reasonable returns in a world filled with increasing volatility and uncertainties, Hong Kong-based Mirae Asset Global Investments has jumped on the Shariah bandwagon by launching its first-ever Islamic product — the Islamic Asia Sector Leader Equity Fund — as it seeks to broaden its appeal to Shariah investors and make further inroads into the universe of Islamic equities. DANIAL IDRAKI explores the new fund.

Mirae’s latest venture, which seeks to achieve long-term capital growth by investing in Shariah compliant companies across Asia (excluding Japan), will be benchmarked against the MSCI Asia ex Japan Islamic Index, and the asset management arm of South Korea’s Mirae Asset Financial Group has appointed Amanie Advisors and IdealRatings as its respective Shariah supervisory board and Shariah stock-screening provider. The Islamic fund is a sub-fund of the Mirae Asset Global Discovery Fund SICAV, a Luxembourg-domiciled UCITS, and Mirae plans to register the fund for public distribution in selected jurisdictions across Asia, Europe and the Middle East.

The Shariah compliant fund will mirror Mirae’s Asset Asia Sector Leader Equity Fund, following in the same investment strategy and process. Jad Shams, the head of MENA of Mirae Asset Global Investments (UK), commented that Middle Eastern investors are increasingly looking to diversify their assets, both in terms of asset class and region. “Our consumer-focused approach in stock selection is proving popular among investors who understand our bottom-up approach,” he noted. Mirae, however, did not disclose the fund’s targeted size or its expected annual yield.

Mirae currently has a presence in 12 countries and over US$100 billion in assets under management worldwide. The firm’s equity investment is divided between emerging markets at 77% and developed markets at 23%. The Asset Asia Leader Equity Fund has a diverse portfolio across a number of sectors including IT, healthcare, consumer staples, energy and telecommunications, while big names in the Asian financial technology universe such as Tencent, Alibaba Group and Samsung Electronics make up the fund’s top ten holdings. Since its launch in 2013, the fund has given a reasonable 14% return as at the end of October 2016, beating the fund’s benchmark — the MSCI AC Asia ex Japan Index — return of 7%, although the fund’s year-to-date return stood at 2.4%, much lower compared to the benchmark’s 11.1%.

Mirae’s Islamic fund comes amid a wave of global investors stepping up its effort to widen its investor base and increase its reach to Shariah investors. In November, Italy-based Azimut Group partnered with Malaysia-based Maybank Asset Management Group (MAMG) to manage the Azimut MAMG Global Sukuk Fund (see IFN Report Vol 13 Issue 47), while Japan’s SBI Holdings is working with the Saudi Arabia-based IDB and the Bruneian Ministry of Finance to launch a seven-year US$100 million Islamic private equity fund (see IFN Report Vol 13 Issue 38).

§

Headquartered in Bahrain and with a growing regional and international presence, wholesale investment bank Securities & Investment Company (SICO) is one of the leading securities houses in the Gulf, as well as managing a number of external Shariah compliant funds including the recently launched Islamic REIT from Eskan Bank, the Al Islamic GCC Equity Fund from Dubai Islamic Bank and the Qatar, Bahrain and Oman components of Riyad Bank’s GCC Islamic Equity fund. CEO NAJLA AL SHIRAWI speaks to IFN regarding her predictions for the upcoming year.

What is your overall outlook for 2017 and what can we expect from the GCC market?

The impact on earnings from structural adjustments and budgetary cuts will continue within the region. However, sector-specific theme plays will be a preferred way of investing. The market will remain volatile, reacting to government announcements, regulatory and structural reforms as well as macro developments.

What can we expect in terms of oil price and impact?

Oil is likely to remain within US$50-55 levels, which is still below breakeven levels of most GCC states. Accordingly, we should expect sovereign issuances and borrowing to continue to plug the deficit. Corporates within the region [are likely to] focus on cost efficiencies to protect margins. The role of active asset managers will remain quintessential to outperform in such an environment, as markets will give opportunities to book profits at high levels and re-enter later at lower levels.

What sectors are you bullish on and why?

We are optimistic on banks, petrochemicals, healthcare and real estate in general. However, the sector themes may differ within each country in the GCC. Banks should benefit from interest rate hikes, which should offset impact from higher provisioning. Healthcare remains a growth sector with considerable expansion in most listed names in the region. Petrochemicals is a global industry and accordingly a bit insulated from local demand-specific headwinds. Although subsidy removal is negative on sector margins due to higher feedstock cost, there are plays within the region that continue to benefit from low feedstock.

Further, real estate in Dubai appears resilient and the theme can be played through blue chips. The telecom sector remains a dividend play although revenue growth will be minimal while costs will be managed through efficiency programs. However, the consumer sector (especially discretionary) will undergo stress in the coming year and should be avoided. Further, stress on the building materials and construction sectors will continue in 2017 and remain a high-risk sector which a fundamental investor should avoid.

What are your top three predictions for 2017?

First, we expect oil to trend higher from a 2016 average of US$45. Our prediction is between US$50-55 for 2017. Second, we expect a further pick up in sovereign issuances for 2017. And finally, we may see asset reallocations from debt to equities and real estate at a global level.

§

While 2016 has seen a volatile and turbulent period in the financial markets, global Sukuk issuance for the year has exceeded some of the estimates made earlier by Islamic finance observers. According to RAM Ratings, global Islamic debt issuance reached US$72 billion as at the end of November 2016, surpassing the rating agency’s projection of US$55-65 billion for the entire 2016. In a showcase of its strength as a global Shariah compliant finance hub, Malaysia retained its top spot with a 41.7% market share, followed by Indonesia at 16.4%, the UAE at 11%, Turkey at 7.1% and Pakistan at 6.7%. DANIAL IDRAKI brings you the story.

The corporate sector, meanwhile, posted a 35.5% year-on-year jump in global Sukuk issuance to reach US$30.6 billion as at the end of September 2016, compared to US$22.6 billion during the corresponding period of 2015. The top three issuers in September 2016 originated from Malaysia, the UAE and Qatar, namely the Public Sector Home Financing Board (US$960 million), Emaar Sukuk (US$750 million) and the State of Qatar (US$720 million) respectively. A total of US$5.9 billion of global Sukuk was issued in the same month. “Large issuances from the financial and infrastructure sectors have been a boon to the Sukuk market, and are likely to remain a key catalyst of future growth,” Ruslena Ramli, RAM’s head of Islamic finance, observed.

The rating agency further noted that in the domestic Malaysian market, a total of RM9.6 billion (US$2.16 billion)-worth of local Sukuk was issued in September, leading to a year-to-date issuance value of RM99.5 billion (US$22.38 billion) in the Southeast Asian Islamic finance powerhouse. Ringgit Sukuk issues were dominated by the financial services and infrastructure and utilities sector. As at the end of November 2016, the issuance value of Malaysia’s domestic Islamic debt securities stood at RM125.3 billion (US$28.19 billion), exceeding RAM’s full year projection of RM100–120 billion (US$22.5–27 billion).

Separately, Moody’s had in September released a report stating that it expects new Sukuk issuance volume for 2016 to be at approximately US$70 billion, as challenging economic conditions in emerging markets and the GCC’s desire to tap conventional liquidity from international investors saw subdued Sukuk issuance during the first half of the year at US$40 billion. Moody’s further noted that it expects contribution by Malaysia, Indonesia and the GCC countries, which account for around 90% of total Sukuk issuance, to remain unchanged going into 2017.

…

RELATED:

Reminder: The Global Banking Crisis Threatens All National Currencies

This Time The Most Embarrassing Thing To Say Will Be “No One Saw This Coming”

______________________________________________

Want Worldwide PEACE and Prosperity. We are the solution we have been searching for... Free People on Earth will solve our crisis and create an era of Creativity. Be Aware; Be Creative; Be Active; Be Free; and then Share it. LOVE & Wholeness AMOR y Paz

Islamic Finance:

The important role of sukuk in the Basel III era

Published on 14 Dec 2015 By Dr. Sutan Emir Hidayat, Director of the MBA Program, University College of Bahrain

The implementation of Basel III rules has created several challenges to Islamic financial institutions (IFIs) especially with regards to capital adequacy and liquidity requirements. Basel III primarily requires all banks, including Islamic banks, to strengthen their capital and liquidity positions by holding higher quality capital, which would enable banks to absorb financial shocks, and maintain higher level of liquidity, which enables banks to reduce their dependency on money market instruments.

[…]

Basel III-compliant sukuk

From the above explanation, it is clear that the implementation of Basel III and IFSB-15 has opened the way for sukuk to be used by Islamic banks and other IFIs as the alternative instrument to comply with regulatory requirements. Certainly, the adoption of Basel III will boost the number of sukuk issuance and their transactions value.

Basel III has already created a new trend in the sukuk market with the birth of so-called “Basel III-compliant sukuk”. There have been nine issuances of such instruments since Basel III’s initial implementation which kicked off in January 2013 with total deals worth more than USD 4.93 billion, according to Annuar (2014).

The first issuance of Basel III-compliant sukuk came from Abu Dhabi Islamic Bank (ADIB) in November 2012, even before the initial implementation of the accord.

Read full: https://blogs.thomsonreuters.com/answerson/the-important-role-of-sukuk-in-the-basel-iii-era/

Please download IMF .pdf document

_____________________________________________________________

De-Dollarization & Currency Wars:

RUSSIA, CHINA, IRAN, PHILIPPINES, TURKEY, EEU, AND OTHERS.

Look closely at the declining demand for USDollars and see what really is happening as most currencies plummet in relation to the U.S. Dollar…

Title: Hackers Hit Russia’s Central Bank, Stealing More Than 2 Billion Rubles

Video posted 02 Dec 2016 by DAHBOO77

Title: Rosneft deal enables RUB advance

Video posted 8 Dec by instaforex

Title: China-UK ties: Young leaders gather in Shanghai to discuss globalization

Video posted 7 Dec 2016 by CCTV News

“Shanghai hosted the sixth China-UK Young Leaders Round Table Discussion on Thursday. This is part of the fourth Meeting of China-UK High-Level People-to-People Dialogue. Eight members of parliament and over 20 young leaders from political, business and scientific research fields gathered to discuss global concerns, including globalization and digital innovation.”

Title: Chinese exporters see both gains and losses as China’s yuan fell to its lowest against US dollar

Video posted 8 Dec 2016 by CCTV News

A different CCTV news report said:

“China’s yuan fell to an almost eight-year low on Wednesday as the strengthening U.S. dollar put more pressure on the currency. The People’s Bank of China set the trading rate of the yuan, also known as the renminbi, at 6.8495 against the dollar, down 0.30 percent from the day before. The yuan has been battered in the past weeks, down to a string of six-year lows in the face of a dollar rising on expectations of sharper U.S. interest rate hikes. President-elect Donald Trump pledged during his campaign to boost spending and slash taxes. Analysts say Beijing is now intervening to prop up the yuan’s sagging value against the surging dollar. Take a listen to how the rise and fall of the yuan affects China’s economy with Zhao Zhongxiu from the University of International Business and Economics, Max Wolff from New York’s New School University and Simon French of Panmure Gordon in London.”

Title: China and Egypt central banks sign 18 billion yuan, three-year currency swap deal

Video posted 6 Dec 2016 by CCTV Africa

“China and Egypt have concluded an 18 billion yuan three-year bilateral currency swap deal. Importers and economists say the move will facilitate trade and improve foreign currency liquidity in cash-strapped Egypt. Egypt’s central bank says the deal with the People’s Bank of China could be extended by mutual consent. China has carried out swaps with more than 30 central banks around the world to increase the use of the yuan as a global reserve currency, and to stimulate bilateral trade. The yuan is traded onshore against 16 major currencies. Egyptian importers say the deal with China will allow them to source yuan directly, facilitating imports from China while reducing demand for dollars and easing pressure on the Egyptian pound.”

Title: Turkish Lira falls amidst political uncertainty

Video posted 08 Dec 2016 by Simon Amon

Title: Money Talks: Turkey’s pro-lira campaign

Video posted 6 Dec 2016 by TRT World

Title: Turkey Calls for CURRENCY WAR Against U.S. Dollar! China and Russia!

Video posted 07 Dec 2016 by The Money GPS ~ Author Exposing the Truth

Title: Turkey Erdogan ask Iran,Russia,China to use lira in tradesدرخواست اردوغان از ایران برای تجارت با لیر

Video posted 05 Dec 2016 by ali javid

“Turkey’s Erdogan urges Russia, China & Iran to trade in local currencies In an attempt to boost the falling lira, Turkish President Recep Tayyip Erdogan has offered to trade with Russia, China, and Iran in local currencies”…

LikeLike

Hugo Salinas Price: Gold & India

How Much Gold Is There in India? by Hugo Salinas Price

http://www.plata.com.mx/mplata/articulos/articlesFilt.asp?fiidarticulo=301

“India is a great example of a country where large amounts of gold are in the hands of the population – 1.3 billion human beings, at least.”

Title: How Much Gold Is There in India?

Video posted 06 Dec 2016 by Silver The Antidote

LikeLike

Anyone tell the Donald and the FED about this. What will happen to the Treasury’s new currency?

LikeLike

This is a international consensus (with the Federal Reserve, IMF, G20, BRICS, and others in agreement for this de-dollarization) for the monetary reset.

LikeLike

Then that does not include the Republic of the united States of America. Thank God.

LikeLike

I am not sure what you think the “Republic of the united States of America” is, but the U.S. Congress and the U.S. President signed the treaty as did the governments in China, Russia, and the other corporate-governments…

Personally, I would rather thank God for the gift of personal sovereignty and knowledge of rights and wrongs in this Age of Deception.

LikeLike

It seems you are a citizen of the United States, therefore you and I have a much different knowledge base of the fraud perpetrated on the people of the Land by those of the Sea and when it started.

If you choose to believe you have a U.S. Congress and a U.S. President that represent you even though the Constitution has been put at ease since since 1933, we have little to converse about. Go pay your taxes like a good little citizen servant of the foreign powers you obey.

,

LikeLike

Whoa, why you made that erroneous leap, to think “It seems you are a citizen of the United States”?

I never made such a claim and please do not think such a thing about me.

Amplifying awareness and sharing truth recognizes that knowledge of the truth makes a man unfit to be a slave.

LikeLike

I do agree, and excuse me for prejudging you. I’m to use to being surrounded by complacent useful idiots.

LikeLike

Okay, no worries.

NICE classic sky blue fins, sweeet 🙂

LikeLike

Thanks it my 57 turquoise bucket list car of 9 years.

FYI, They took him away from us for doing the right thing https://youtu.be/ULu5M9D2I-Y

LikeLike

A note to ponder.

When people claim they were a citizen of the USA after the War of Independence they gave up God’s Laws, Natures Laws with the foundation for doing no harm to another, the Soil, the Water, the Air, and all of the Creators Creations on the Land and Seas. They instead choose to honor man made laws of the Esquires that signed the constitution with oversight of the Royal Crown for enforcement. They even gave up the 10 commandments as a basic civics guide for how to get along with your neighbors. Citizen Debt Slaves they all became.

LikeLike

That is true, but that has nothing to do with me personally.

Somehow, you may have misunderstood what I said.

I fully accept nature’s law and reject debt slavery.

Noncompliance to fraud and tyranny is the right choice for sovereign individuals.

LikeLike

Institutional governance has a lot to hide, worldwide from the citizens…

What is “institutional governance”?

Institutional governance is the establishment, it is the authority, the rules of law, the legal system, the state, the government, corporation, formal education, conventional science, religion (which ever formal belief system that claims itself as a religion and qualifies for legal recognition)…

It is civilization, and it is a Mind Trap.

LikeLike

Scripting Monetary Policy:

Banking has more changes coming beside the gold reserves and de-dollarization.

The digital labor, digital currency and the cashless society agenda is revealed in the development of FINTECH or Financial technology…

Title: cashless Australia next As Trump’s killer master plan to defeat the NWO

Video posted 15 Dec 2016 by Silver The Antidote

Title: Cryptocurrency & blockchain update, Bitcoin $1000? which web bot predicts! silver & gold to soar

Video posted 15 Dec 2016 by Silver The Antidote

LikeLike